Key Takeaways:

- Solana perpetual futures funding rates have flipped negative, indicating excess demand for bearish positions.

- Competing networks such as Base and Hyperliquid are aggressively seizing DEX market size, posing a direct threat to Solana.

Solana’s native token SOL (SOL) is facing a 15% correction after being rejected at $98 on May 11. After a retest of the $83 level on Tuesday, a negative futures funding ratio emerged, indicating increased demand for SOL short positions.

While reduced network activity has caused prices to fall, competition between competing blockchain networks has increased.

The annual funding rate for SOL perpetual futures. source: lightness

The SOL perpetual futures funding rate was -3% on Tuesday, significantly down from +8% on Saturday. In neutral market conditions, this indicator hovers around +9%, taking into account cost of capital and exchange rate risk. The demand for bullish leverage has all but disappeared since Saturday, when the price of SOL fell below $90.

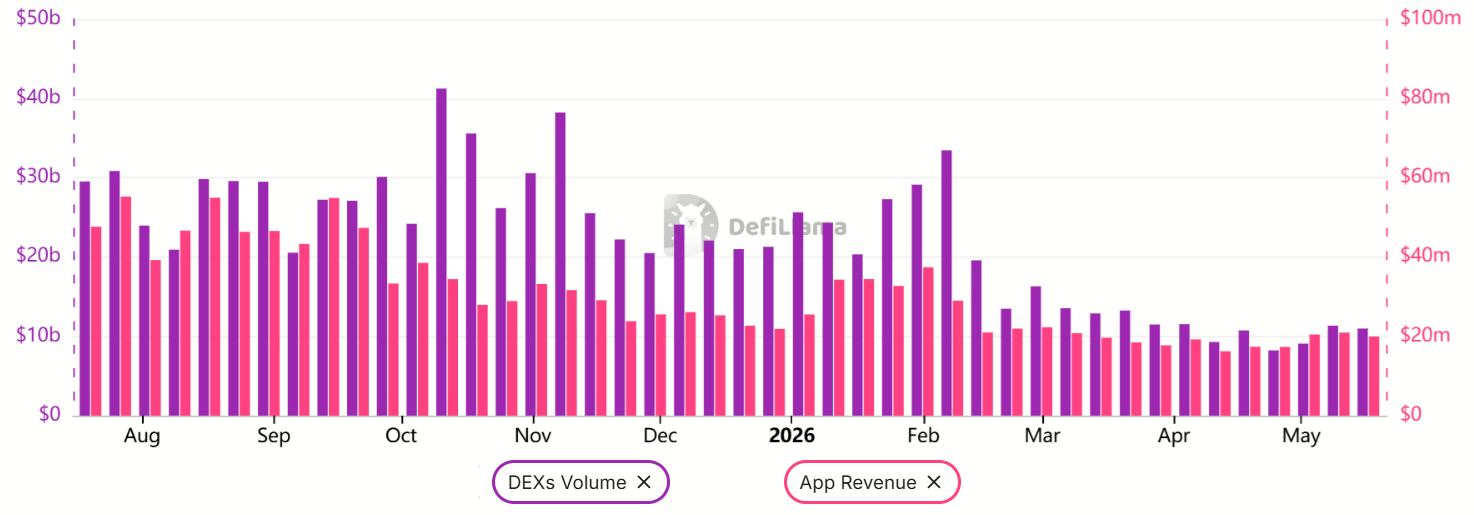

Solana DEX activity has decreased by 56% since January.

The decline in Solana’s decentralized exchange (DEX) activity has resulted in lower ecosystem revenue and SOL demand. The decline in demand for decentralized applications (DApps) was not Solana’s only problem, but increased competition posed a major threat as investors feared that demand for memecoins would decline forever.

Solana Weekly DEX Trading Volume, DApp Revenue, USD. Source: DefiLlama

Solana DApp revenue has stabilized at close to $20 million per week, down from an average of $35 million in January. This move closely reflects trends in the network’s DEX activity, which currently stands at $11 billion per week, compared to an average of $25 billion in January. Solana’s 30-day DApp revenue leaders are Pump, Axiom Pro, Phantom, and Jupiter, which together have a 65% market share.

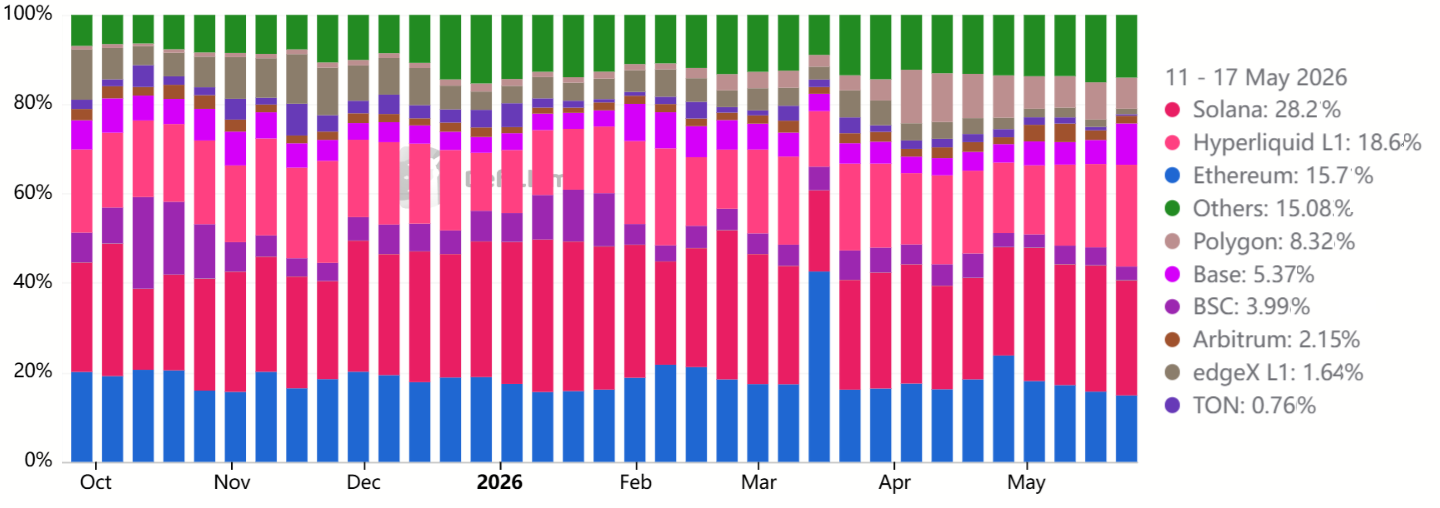

Blockchains ranked by weekly DApp revenue market share. Source: DefiLlama

Solana remains the leading blockchain in terms of DApp revenue despite fierce competition. Hyperliquid poses an immediate threat for the following reasons: Dominance of Perpetual ContractsIt provides a high-throughput solution with core transaction functionality built directly into the consensus layer. Meanwhile, the Ethereum layer-2 network Base provided seamless integration into the Coinbase ecosystem.

In terms of Total Locked Value (TVL), Solana ranked second with $5.9 billion, followed by BNB Chain with $5.5 billion and Base with $4.5 billion. DEX platforms and staking DApps such as Jupiter, Kamino, Sanctum, and Raydium are leading Solana’s TVL. Still, no blockchain threatens Ethereum’s $43.2 billion TVL, which relies heavily on collateralized lending and liquid staking.

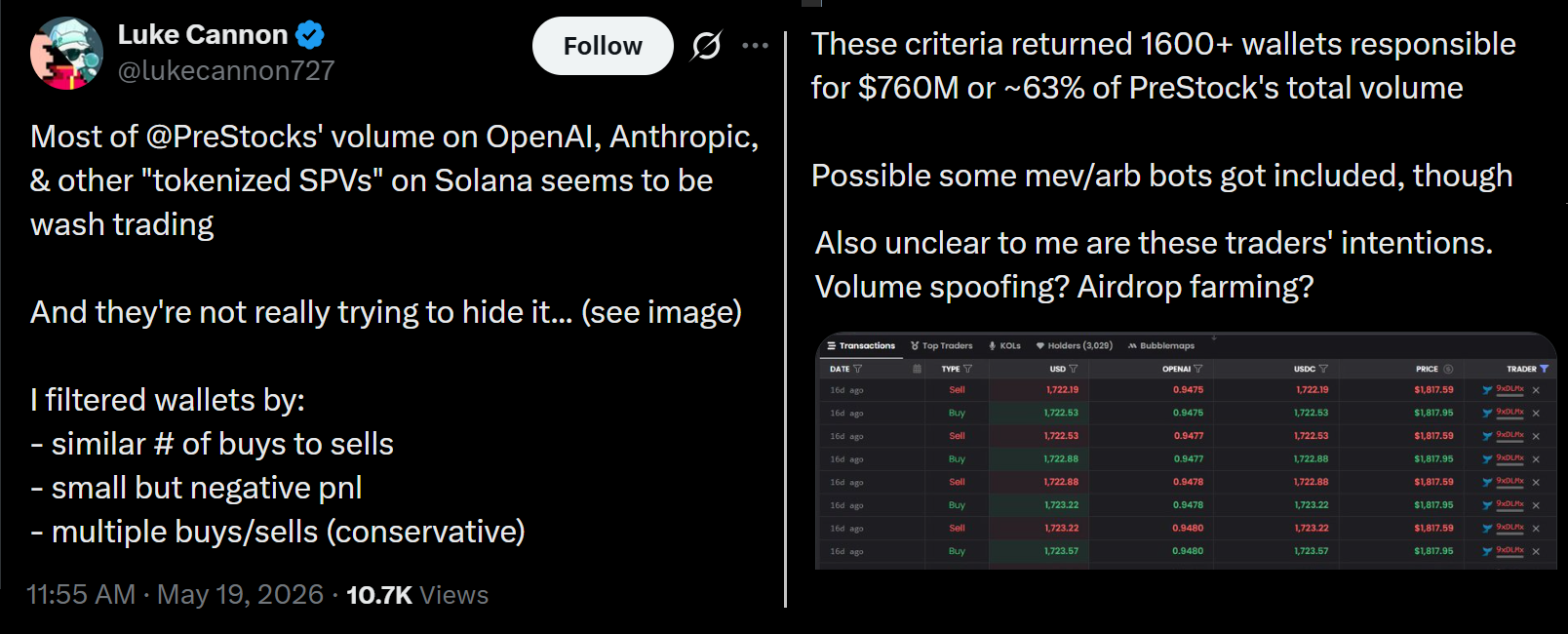

Potential spoofing activity on Solana Network DApps

Solana’s presence in the DApp industry cannot be underestimated, but the network’s low fees provide the perfect opportunity for maximum extractable value (MEV) botting and inflated activity.

relevant: Goldman Sachs Ends XRP, Solana ETF Exposure in Q1 2026

Source: X/Luke Cannon 727

X user lukecannon727 said 1,600 addresses are reportedly responsible for nearly 63% of trading volume on PreStocks, a synthetic asset trading platform running on the Solana network. Our analysis shows that these companies exhibit balanced trading activity, high execution frequency, and small net losses. These findings are highly consistent with arbitrage activity, but may also indicate volume spoofing.

The recent weakness in SOL prices can be partially attributed to a widespread decline in DApp demand and increased competition, particularly from Hyperliquid and Base. An eventual bull market appears to be heavily dependent on a recovery in DEX activity, especially in memecoin trading. But at the same time, there is no indication that SOL needs to retest the $78 level last seen in early April.